Returns Overview

EPS is the opium of the executive suite; it is the Don Juan of corporate value.

What do we mean by Returns?

Returns are the defining idea of business, determining wealth creation at an individual, firm and economy wide level. They are arguably the most important fundamental driver of share prices. The concept is fairly simple.

Return on Investment (Returns for short), refers to the net amount of money we get back on any investment project:

- The total dollar amount of return: Cash Out less Cash In

- The rate of return per dollar invested: Cash Out/Cash In

Why do we analyse Returns?

We analyse returns to in order to understand how a company creates value. This knowledge then applies to the secondary questions of:

- Valuation;

- Company operating performance; and

- Management Performance

The Level of Profitability¹ (returns) is the key driver of value creation – the more a project gives back for a given investment the better. Therefore, companies that can invest in such projects create more value. A simple example shows this process at work.

Example: One Period Growth Model

Consider two companies that both have the same current level of earnings (cash flow). The difference between the companies is that Company 1 Invested $100 to generate this $10, whereas Company 2 only had to invest $10 to generate the same $10 cash flow.

In a static world, where nothing changes, both of these companies would have the same value. Investors are only interested in future cash flows, so at a cost of capital of say 8% (valuation multiple = 10/0.08 = 12.5) both companies in this scenario would have a value of $125 (10 x 12.5).

However, what if these companies exist in a growing industry and continue to invest in their operations to expand? Assuming a doubling of both businesses, each company would then have a gross value of $250 (=20/0.08).

However, there is a key difference in the path taken to acheive this growth.

Company 1 had to invest an additional $100 in capital to double the business, whereas Company 2 only required $10 in incremental capital. The gross value of the businesses is the same post growth, but the net value (which is what shareholders would experience), is quite different.

Gross v. Net Value

This is a simplified one period growth model, but the same idea holds if we assume that reinvestment is a continuous process. This is the genesis of the Dividend Discount Model.

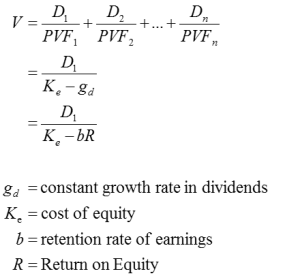

Example: Dividend Discount Model.

The DDM is a continuous version of the one period model above which describes how value is created (or destroyed) by the retention and reinvestment of dividends.

At rates of return above the discount rate, higher retention rates create value, whilst the opposite is true at rates of return below the discount rate.

Both the one stage growth model and the perpetual growth model encapsulated in the DDM are simplifications. However, they demonstrate two powerful investing truths:

- In order to create value, we must get back more than we put in. If the cost of the money we invest is greater than the return wealth is destroyed.

- The level of returns only matters if we are investing. In a static environment, high returns and low returns are theoretically identical because the investment has already occurred and investors are only interested in the cash that is still to come out. In fact, for low growth companies in the real world, high returns may actually be worse than low returns because they may indicate that the trend of profitability is more likely to be negative.

How do we measure Returns?

The conceptual measurement of returns is easy. We simply have to add up the amount of cash in and the amount of cash out to create either a measure of the absolute dollar return:

Cash Out – Cash In

… or the relative return:

Cash Out/Cash In

But there are a number of obvious complications with this process which ultimately have a large bearing on which measure of return to use and how to interpret it. Broadly stated, these problems are:

- The need to adjust for the timing of cash flows.

- The need to adjust for the risk of the cash flows.

- How to measure the cash in.

- How to measure or forecast the cash out.

As a result of these problems, analysts use a wide range of tools to measure returns. These various tools deal with the major problems in different ways.

When is Returns Analysis important?

Although arguably the most important of the analytical tools, returns analysis still needs to be put in context so it can help us understand the investment system. For investors, the key contextual considerations for returns revolve around the following questions:

- Fundamental valuation

- Operating Performance of the business

- Management Performance

For each of these questions, we also need to recognise that the complexity of the real world involves a mix of sunk capital and future investment opportunities, such that value is the combination of:

Trend in Returns from Existing Capital + Value Creation from Future Deployment of Capital

As a result, investment markets are usually more sensitive to the change in returns than they are to the level of returns. To measure this trend properly we need to:

- Distinguish between the profitability of existing capital and the potential to deploy further capital.

- Make sure we are measuring the true trend in profitability, rather than a manufactured accounting artifact.

And finally, each of these questions must then be considered along with an understanding of:

- Where it fits in the individual investing framework; and

- What else is relevant to that framework.

Summary – Returns Analysis

To summarise, returns are the key to how investments create value. Our first step is to understand the key tools we have for measuring returns and their respective strengths and weaknesses:

Measuring Returns

General Returns Measurement Considerations

- Accounting Profits – EPS, NPAT, EBIT, EBITDA

- Accounting Returns – ROE, ROA, ROFE

- Discount Functions – IRR, NPV

- Economic Returns – EVA, CFROI

- Marginal Returns – Dupont Model, Other Incremental Return Models

The second step is to place these measures into context to help us answer the questions relevant to our investment framework.

Returns in Context

- Cyclical v. Growth

- Sustainability

- Industry Context